Bullion Banks and the Future of Indonesia’s Gold Economy

Mohammad Nur Rianto Al Arif

(Professor at UIN Syarif Hidayatullah; Secretary General of the Indonesian Lecturers Association; Executive Board Member of IAEI; Executive Board Member of ISEI Jakarta Chapter)

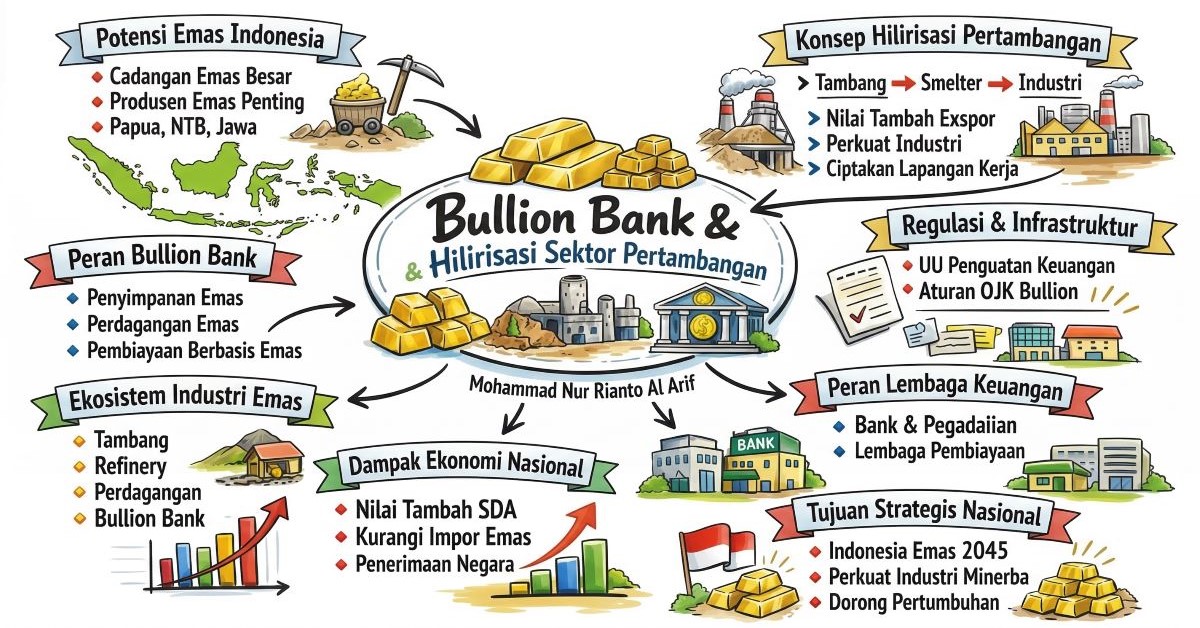

In recent years, the downstreaming of natural resources has become one of Indonesia’s main economic development strategies. The government aims to ensure that natural wealth is no longer exported merely as raw materials but processed domestically to generate greater added value for the national economy.

So far, downstreaming has mostly been discussed in the context of commodities such as nickel, bauxite, and copper. However, there is another strategic commodity that is equally important: gold.

As a country with significant gold reserves, Indonesia has the opportunity to develop a more integrated gold industry, from mining to the financial sector. In this context, the idea of a bullion bank has emerged—a financial institution that provides gold-based services such as gold savings, gold-backed financing, and gold trading.

In February 2025, the Indonesian government officially launched bullion bank services operated by financial institutions such as Pegadaian and Bank Syariah Indonesia after receiving approval from the Financial Services Authority (OJK). The presence of bullion banks is expected to strengthen the national gold ecosystem, reduce dependence on gold imports, and support the downstreaming of the domestic gold mining industry.

The presence of bullion banks is not only about financial sector innovation but also part of a broader mining downstream strategy. Moreover, if properly designed, bullion banks can align with Islamic economic principles, particularly in promoting fair resource management and broader public benefit.

Indonesia is among the countries with large gold potential globally. Data from various international institutions show that Indonesia’s gold reserves reach around 2,600 tons, placing it among the largest in the world.

Indonesia also hosts world-class gold mines, including those operated by PT Freeport Indonesia in Papua and various mines owned by PT Aneka Tambang (Antam).

However, this large potential does not always translate into economic value for the country. In many cases, gold is still treated mainly as a mining commodity. After extraction, it is often exported or traded in forms that do not maximize domestic added value.

This reflects a common paradox in resource-rich countries: abundant natural wealth, but limited economic benefits for society. Therefore, downstreaming is crucial to ensure that the mining value chain does not stop at resource extraction.

In the case of gold, downstreaming is not only about refining the metal into industrial products but also integrating it into the national economic and financial system.

In modern economies, value is created not only in production but also in finance. This also applies to gold. Besides being used in jewelry and manufacturing, gold functions as an investment asset and a global financial instrument.

This is where bullion banks play a strategic role. A bullion bank manages gold-based economic activities, including storage, trading, and financing. Through this institution, gold becomes part of the financial intermediation system.

In this sense, bullion banks can be seen as financial infrastructure for gold downstreaming. If smelters process minerals into metals, bullion banks integrate those metals into the broader economy. Gold that was previously stored passively can be used for productive economic activities, extending the domestic gold value chain.

The economic potential of Indonesia’s gold industry is substantial. Studies estimate that the total value of the national gold business chain reaches around Rp482 trillion per year. This includes mining, refining, jewelry, trading, and gold-based investment.

If this ecosystem is managed more effectively, the gold industry’s contribution to the national economy could increase significantly. Some analyses suggest that developing a bullion bank ecosystem could boost GDP by around Rp245 trillion and create more than 1.8 million jobs in the long term.

These figures show that gold is not just a mining commodity but a broad source of economic activity. However, this potential can only be realized if the value chain is strengthened from upstream to downstream.

In Islamic economics, gold holds a very important position. Since early Islamic civilization, gold was used as currency in the form of dinars, while silver was used as dirhams. Both served as relatively stable standards of value.

However, Islam views gold not only as a medium of exchange but also as a trust (amanah) that must be managed fairly for the benefit of society. This aligns with the concept of maqasid al-shariah, which emphasizes welfare and economic justice.

In this context, gold management should not stop at extraction. It must be optimized to generate broader economic benefits through industry, trade, and finance.

Bullion banks can serve as instruments to achieve this. By integrating gold into the financial system, it becomes an active asset that supports productive economic activities.

For Indonesia, which has a rapidly growing Islamic finance industry, bullion banks also open opportunities for developing gold-based Islamic financial instruments.

One characteristic of Indonesian society is a strong preference for gold as an investment. Many households store gold in the form of jewelry or bullion as long-term savings. However, most of this gold remains stored informally at home, meaning it is not used for productive economic activities.

Bullion banks can bridge this gap by integrating privately held gold into the formal financial system. This allows gold to function not only as a store of value but also as a source of economic financing. In Islamic economics, this aligns with the principle of tadawul al-amwal, or the circulation of wealth within the economy.

Despite its potential, the development of bullion banks faces several challenges. First is gold price volatility. Although gold is relatively stable in the long term, it can fluctuate in the short term.

Second is regulatory and governance challenges. Bullion banking is a new concept in Indonesia’s financial system and requires a strong regulatory framework.

Third is the risk of market speculation. Without proper oversight, gold trading could lead to instability. In Islamic economics, excessive uncertainty (gharar) and speculation (maysir) must be avoided.

Therefore, bullion bank development must ensure that all activities remain aligned with sharia principles.

At its core, bullion banking is an innovation that brings gold out of vaults into the productive economy. In the context of mining downstreaming, it extends the value chain from extraction to finance.

However, success depends not only on the existence of bullion banks. Gold downstreaming requires a comprehensive approach, including strengthening mining, expanding refining capacity, and developing gold-based financial markets.

From an Islamic economic perspective, gold management must aim to create broader economic welfare. Gold is not just a commodity or investment instrument but a trust that must be managed fairly and productively.

If downstreaming strategies are implemented consistently and bullion banks are managed properly, Indonesia has a strong opportunity to become a major gold trading hub in Asia.

Ultimately, the success of this policy is not measured by how much gold is mined but by how much economic value and social benefit it generates for society. In that sense, bullion banks can become a key instrument in building a more sovereign, inclusive, and just national economy.

This article was published in CNBC Indonesia on Tuesday, March 17, 2026.